》Check SMM's spot aluminum quotes, data, and market analysis

》Subscribe to view historical price trends of SMM's metal spot cargo

SMM News on May 6, 2025:

According to SMM data, the average tax-inclusive full cost of China's aluminum industry in April 2025 was 16,386 yuan/mt, down 3.7% MoM and 0.9% YoY, mainly due to the significant pullback in alumina prices during the period. SMM data showed that the monthly average SMM Alumina Index during the period (March 26-April 25) was 2,954.95 yuan/mt, down 10.62% MoM. The average spot price of SMM A00 aluminum in April 2025 was approximately 20,074 yuan/mt (March 26-April 25), with domestic aluminum industry averaging profits of about 3,688 yuan/mt.

As of the end of April 2025, the operating capacity of domestic aluminum reached 43.91 million mt, and the industry's highest full cost fell to 19,218 yuan/mt. If the industry uses the monthly average price for measurement, 100% of domestic aluminum operating capacity was profitable in April.

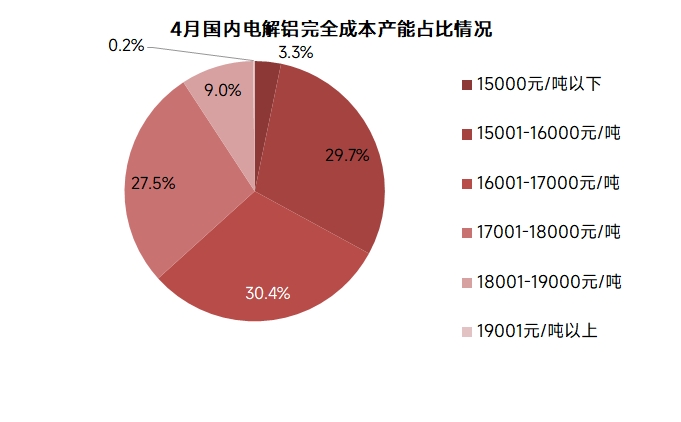

From the perspective of the cost distribution range of aluminum capacity:

The overall distribution range of aluminum's full cost in April shifted downward. In April 2025, the lowest full cost of aluminum was approximately 13,289 yuan/mt, and the highest was approximately 19,218 yuan/mt. In March, the lowest full cost was approximately 13,865 yuan/mt, and the highest was approximately 20,089 yuan/mt. The capacity distribution was as follows:

In March, the capacity with a full cost below 15,000 yuan/mt accounted for 3.3%;

The capacity with a full cost in the range of 15,001-16,000 yuan/mt accounted for 29.7%;

The capacity with a full cost in the range of 16,001-17,000 yuan/mt accounted for 30.4%;

The capacity with a full cost in the range of 17,001-18,000 yuan/mt accounted for 27.5%;

The capacity with a full cost in the range of 18,001-19,000 yuan/mt accounted for 9.0%;

The capacity with a full cost exceeding 19,001 yuan/mt accounted for 0.2%.

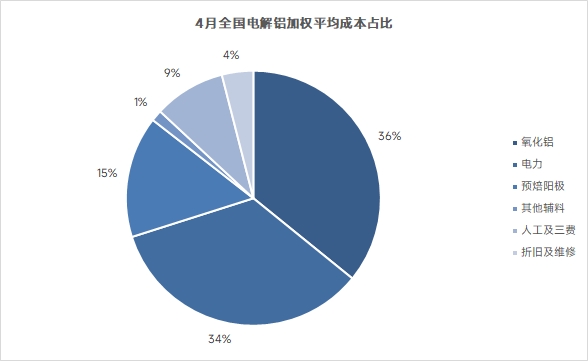

Cost side, from the perspective of cost breakdown:

In terms of alumina raw materials, according to SMM data, the average SMM Alumina Index in April was 2,955 yuan/mt (March 26-April 25). The weighted average cost of alumina for the national aluminum industry in April decreased by 10.4% MoM, accounting for 39% of aluminum's full cost. Currently, with the commissioning of new capacity and the resumption of maintenance capacity, alumina's operating capacity has rebounded significantly, increasing by 3.48 million mt/year on a WoW basis. In the short term, some alumina refineries have plans for maintenance and production cuts, but at the same time, new alumina capacity will further ramp up production, and alumina's operating capacity may fluctuate slightly. Overall, the tightening of alumina spot supply caused by concentrated maintenance and production cuts in the early stage is expected to ease somewhat, and short-term prices are expected to continue fluctuating downward.

In terms of auxiliary materials, the price of prebaked anode continued to rise in April, primarily due to the fact that although the price of raw material petroleum coke showed a weakening trend, it remained at a high level, providing strong cost support. Regarding aluminum fluoride, the cost of raw materials remained high, and the contraction trend on the supply side continued, prompting a significant increase in aluminum fluoride prices in April. The combined effect of these two factors directly drove up the production cost of aluminum in April. Entering May, the market landscape changed. Affected by the continuous decline in prices due to weak downstream demand in the raw material market for prebaked anode, it began to fall. The aluminum fluoride market also faced significant downward pressure on prices due to the continuous decline in cost side. Overall, it is expected that the auxiliary material market will show a downward trend in May, which will drive down the production cost of aluminum simultaneously.

In terms of electricity prices, electricity prices remained stable overall in April. In some regions, the decline in coal prices led to a decrease in electricity costs. The national average electricity price in April fell slightly, with electricity costs accounting for 34% of aluminum's full cost. Entering May, electricity prices are expected to remain stable, and subsequent attention should be paid to the changes in electricity price reductions after the south-west China enters the rainy season.

Entering May 2025, the monthly average price of alumina continues to decline; auxiliary material costs are falling; electricity costs remain stable. Overall, the cost of aluminum is expected to show a downward trend. In summary, SMM expects that the average tax-inclusive full cost of China's aluminum industry in May 2025 will be around 16,000-16,400 yuan/mt.

Data source: SMM Click on SMM's industry database for more information

(Mingxin Guo 021-51595800)